》View SMM Silicon Product Prices

》Subscribe to View Historical Price Trends of SMM Metal Spot

In 2025, the backsheet market started the year with the industry continuing to fluctuate downward. Market demand remained persistently sluggish, coupled with some downstream module manufacturers further reducing single-glass module capacity in 2025. Overall, the demand for backsheet products weakened further, and the shrinking market demand has led some top-tier enterprises in the backsheet sector to plan to moderately reduce their operating capacity in 2025. Additionally, as most backsheet manufacturers are also involved in encapsulant film or other business segments, many backsheet enterprises are expected to focus more on other product segments in 2025.

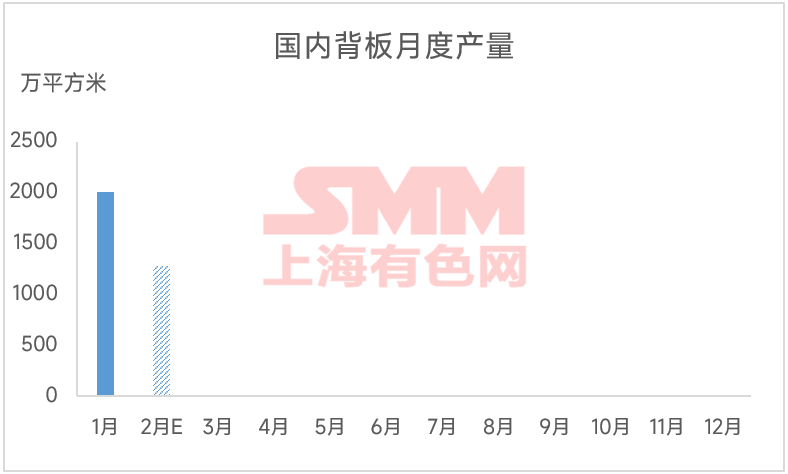

According to the latest processing data from market feedback, backsheet production in January 2025 remained at a relatively low level, with the industry's operating rate still around 10%. Amid the continued sluggish and weak backsheet market, some manufacturers that shut down conventional backsheet production lines in 2024 still have no production resumption plans in the near term. Currently, conventional backsheet prices remain below cost levels, and enterprises show low willingness to sign orders with further price concessions. Coupled with muted downstream demand, the market is generally characterized by a situation of prices without transactions.

Based on feedback from various market enterprises, it was found that the total backsheet production in January was slightly more optimistic than expected. This was mainly due to the impact of the Chinese New Year holiday in January, as many overseas module enterprises had a habit of stockpiling before the holiday, leading to a slight rebound in backsheet procurement activity. The increase in overseas orders drove a rise in total backsheet production. The actual production in January was around 20 million square meters, but the total volume still remained at a relatively low level, with the industry's average operating rate still hovering around 10%.

However, after the Chinese New Year, most enterprises reported that backsheet order transactions in February were average. Currently, orders on hand are limited, and based on these orders, it is estimated that the total production and sales in February may see a significant decline compared to January. Most enterprises expect February's production schedule to drop by more than 30% compared to January. The overall sentiment in the industry remains predominantly pessimistic.

![[SMM PV 뉴스] 화넝의 90MW 태양광 발전 프로젝트 착공!](https://imgqn.smm.cn/usercenter/EaYRd20251217171743.jpg)

![[SMM PV 속보] 징코솔라, '써니 365' 스마트 PV+ESS 시스템 출시: 제조업용 PV+ESS 통합 솔루션](https://imgqn.smm.cn/usercenter/xBtJB20251217171738.jpg)

![[SMM PV 뉴스] 중앙 국유 기업 지속 인정! Risen Energy 하이퍼이온 프로, 다탕 위광 프로젝트 계통 연계 지원](https://imgqn.smm.cn/usercenter/FmBvY20251217171737.jpg)